Asset Allocation has been part of the investment professional’s asset management strategy for decades. More recently, a considerable amount of attention has been focused on a natural extension of that approach: Asset Location.

KEY TAKEAWAYS

Asset location is an investing strategy that has potential to lower your clients’ overall tax bill.

- There are taxable, tax-deferred, and tax-exempt accounts.

- Potentially improve the tax efficiency of investments by putting investments in tax-deferred or tax-exempt accounts instead of taxable accounts.

- While ‘Allocation’ and ‘Location’ are extremely similar, the meanings are quite different:

Asset Allocation: The selection of a diversified portfolio of stocks, bonds, cash, and alternatives aligned with an investor’s time horizon and risk tolerance.

Asset Location: The placement of assets in taxable, tax-deferred, and tax-free accounts with the goal of minimizing taxes

WHERE IS ASSET LOCATION BEING TALKED ABOUT?

A quick Google search uncovers any number of hits from asset managers and the like, but if we look at where most consumers may ultimately go for information on a topic like this once they are exposed to it, two sources stand out:

- Investopedia1

- Fidelity 2

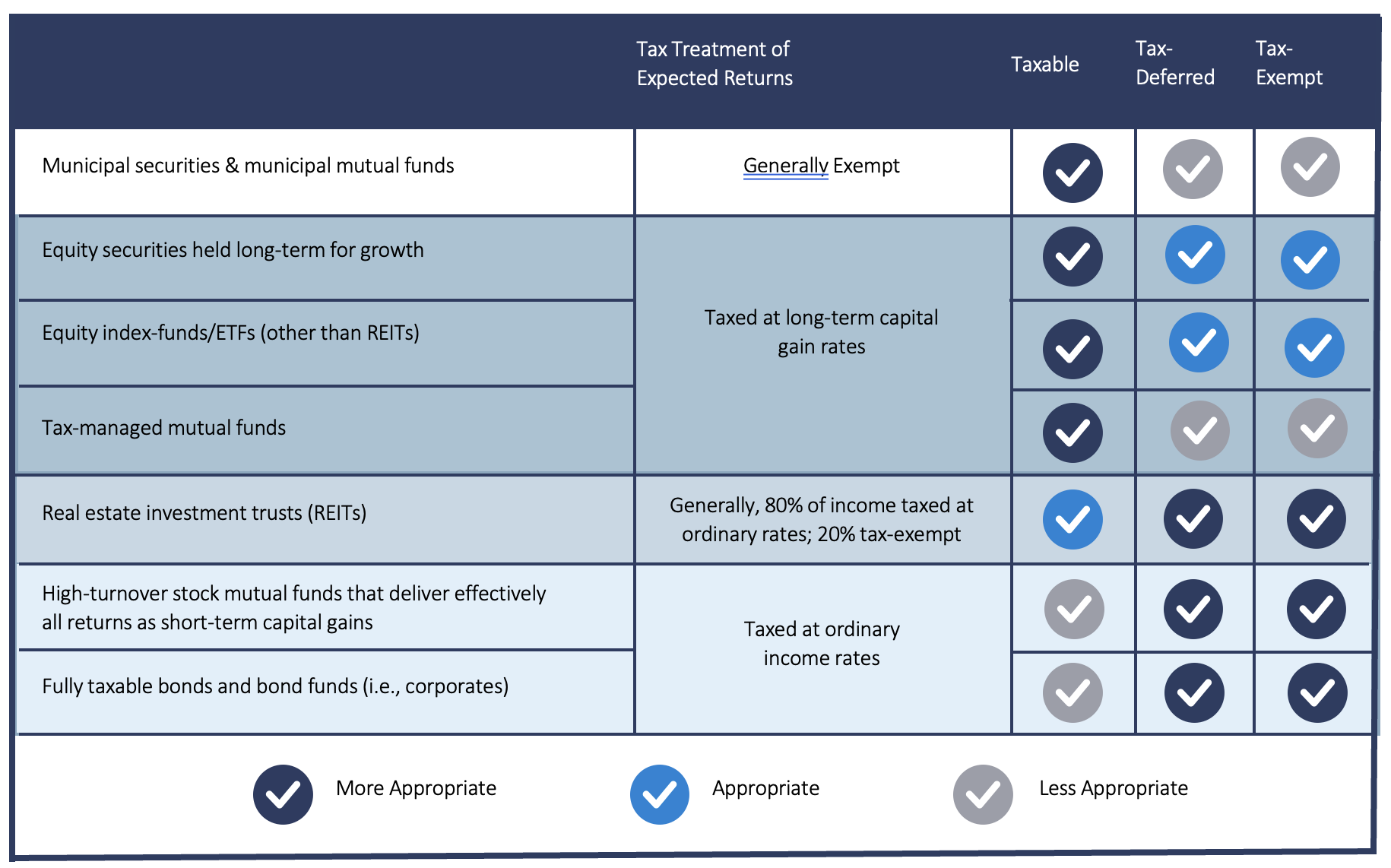

Fidelity goes so far as to outline the tax treatment of various assets as part of their effort to educate their clients as seen in Figure 1.

FIGURE 1

You’ll likely notice one very important omission in both of those articles and Figure 1: Both Fidelity and Investopedia have neglected an asset class that should play a large role in the Asset Location conversation: Cash Value Life Insurance.

This omission is not just common, it’s nearly universal. The asset management community largely has no idea how life insurance fits in the approach they already embrace and are using with clients.

We’ve known for years that life insurance’s unique value proposition positions it as an analog to things like Roth IRAs that have the following characteristics regarding taxation —tax-free: will be invested after tax, but you will not pay taxes on any distributions from these assets.

Of course, life insurance has a significant advantage: the income-based limitations that can prevent clients from utilizing Roth IRAs don’t exist for life insurance.

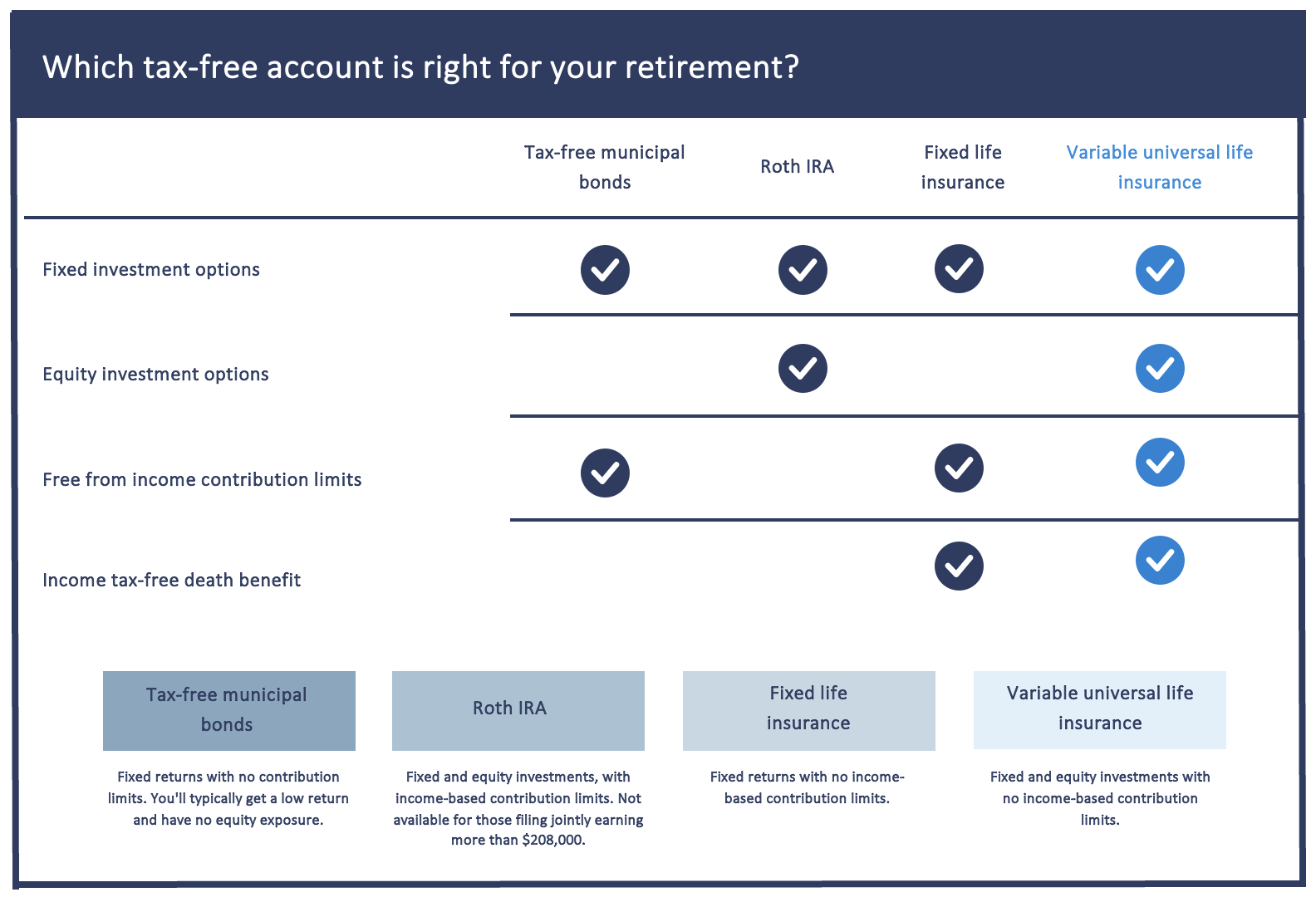

If we investigate the account types that fall into the tax-free category further, as seen in Figure 2, the advantages of life insurance over alternatives become even clearer.

ASSET LOCATION – FIGURE 2

Each tax-free account has different benefits

There are four main types of financial accounts that produce tax-free income: municipal bonds, tax-exempt, Roth IRAs, fixed life insurance, and variable universal life insurance.

WHAT’S THE BOTTOM LINE?

In short, positioning cash value life insurance as a tax-free product in an asset location strategy is an ideal way to introduce clients to the unique tax treatment of life insurance. It solves a challenge they face in terms of income-based limitations and the like that can prevent them from utilizing more traditional tax-free assets that offer market returns.

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.

JOSHUA RHEM

VICE PRESIDENT – LIFE SALES

Joshua Rhem has over 15 years of experience in Insurance and Investment services, with experience as an RIA to financial institutions, an insurance producer, and wholesaler. Throughout his career Joshua has always been especially interested in making sure that insurance is viewed as a vital component of a well-constructed comprehensive financial plan. Understanding the obstacles that advisors face each day, Josh is eager to support them, and promptly responds to their needs. He enjoys helping advisors, brokers and agents grow their business with strategies to identify opportunities and helping to effectively position insurance products as meaningful solutions to their clients’ financial goals.