Case Study Analysis: After 5 Years

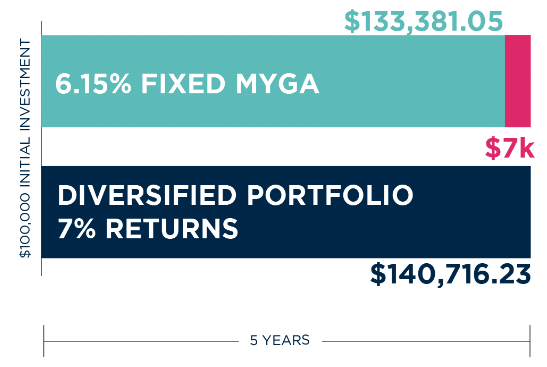

At the end of the period, the MYGA is worth $133,381.05 while the Diversified Stock Portfolio is worth $140,716.23. You’ve got to ask yourself — and your client — if the $7k gained is worth the risk?

In this scenario, the diversified stock portfolio offers the potential for higher returns and, on average, could outperform the MYGA. However, it also carries a higher level of risk and volatility. The MYGA, while offering a lower return, guarantees a stable 6.15% interest rate for the entire five-year period, providing a level of safety that the stock portfolio cannot match.

Risk premium is a way to measure the risk associated with various types of investments and serves as compensation for investors who tolerate the extra risk. It’s one of the key factors considered when deciding where to put money to work.

4 Reasons Why MYGAs Should Be a Part of Planning

The choice between the MYGA and the diversified stock portfolio depends on the client’s risk tolerance, financial goals, and investment horizon. But beyond that, here are some reasons why MYGAs should be considered as a valuable component of financial planning:

- Capital Preservation: MYGAs guarantee the safety of the principal amount invested, which is especially appealing to risk-averse clients who prioritize capital preservation over higher returns.

- Predictable Returns: The MYGA’s fixed 6.15% interest rate provides predictable returns, making it a reliable option for clients seeking stability in their investment portfolio.

- Diversification: Diversifying a portfolio by including MYGAs alongside riskier assets helps mitigate downside risk and create a balanced investment strategy.

- Customized Risk Exposure: Advisors can use MYGAs to fine-tune a client’s risk exposure, aligning their investments with their unique risk tolerance and financial objectives.

Risk premium is a crucial concept in financial planning. This case study demonstrates the importance of considering MYGAs in the context of financial planning. While at-risk assets may offer the potential for higher returns, MYGAs provide safety, predictability, and capital preservation. If you’re looking for creative ways to maximize MYGAs, consider a laddering structure. Regardless, including MYGAs as part of a diversified portfolio can help clients achieve a well-balanced risk-return profile while safeguarding their financial future.

Erick

VP of Annuity Sales

Erick Lindewall is an industry veteran with 30 years of experience, including over 20 years as an External Variable Annuity Wholesaler. He as worked with financial advisors in all major distribution channels. Erick has been recognized as a sales and relationship management leader multiple times during his wholesaling career.