9.46% is the Taxable Equivalent Yield needed to match a 6.15% Tax Deferred Yield in a non-qualified account.

KEY TAKEAWAYS

- Taxable Equivalent Yield is a useful tool for advisors to help clients compare the impact of taxes on investment returns and tax-deferred alternatives.

- Combining federal and state income tax rates can lead to higher TEY with tax-deferred products, such as MYGAs.

- Key Formula: TEY = Taxable Yield / (1 – Tax Rate)

- Clients may forget that the yield on a tax-deferred product is not directly comparable to the yield on a taxable security.

When it comes to investing, a key consideration is the yield (or return) expected on investments. It’s important to understand that not all yields are created equal, especially when taxes are involved.

Taxable Equivalent Yield (TEY) is a concept that can help you compare the returns on different investments, taking into account their tax implications. In this blog, we’ll explore how Taxable Equivalent Yield works and what the TEY needs to be at different tax brackets to equal a 6.15% tax-deferred yield on a MYGA (Multi Year Guaranteed Annuity) that is currently available (talk with your DMI Annuity Specialist for product information).

A client may forget that the yield on something tax-exempt or tax-deferred is not directly comparable to the yield on something taxable.

WHAT IS TAXABLE EQUIVALENT YIELD (TEY)?

TEY is a measure used to compare the yield of a taxable investment to that of a tax-deferred or tax-exempt investment. It helps investors make informed decisions by accounting for the impact of taxes on their investment returns.

To calculate the TEY, you first need to know the yield of the taxable investment and the tax bracket. The formula for TEY is as follows:

TEY = Taxable Yield / (1 – Tax Rate), with the tax rate is expressed as a decimal.

TAX BRACKETS AND TEY

10% Tax Bracket

The TEY calculation would be: TEY = Yield / (1 – 0.10)

Solving for Yield:

Yield = 6.15% / (1 – 0.10)

Yield = 0.0615 / 0.90

Yield = 0.0683 or 6.83%

In the 10% tax bracket, your taxable investment would need to yield approximately 6.83% to be equivalent to a 6.15% tax-deferred yield.

The higher the tax bracket, the greater the taxable yield needs to be to match the return of a tax-deferred investment or product.

22% Tax Bracket

The TEY calculation would be: TEY = Yield / (1 – 0.22)

Solving for Yield:

Yield = 6.15% / (1 – 0.22)

Yield = 0.0615 / 0.78

Yield = 0.0788 or 7.88%

In the 22% tax bracket, your taxable investment would need to yield approximately 7.88% to be equivalent to a 6.15% tax-deferred yield.

35% Tax Bracket

The TEY calculation would be: TEY = Yield / (1 – 0.35)

Solving for Yield:

Yield = 6.15% / (1 – 0.35)

Yield = 0.0615 / 0.65

Yield = 0.0946 or 9.46%

In the 35% tax bracket, your taxable investment would need to yield approximately 9.46% to be equivalent to a 6.15% tax-deferred yield.

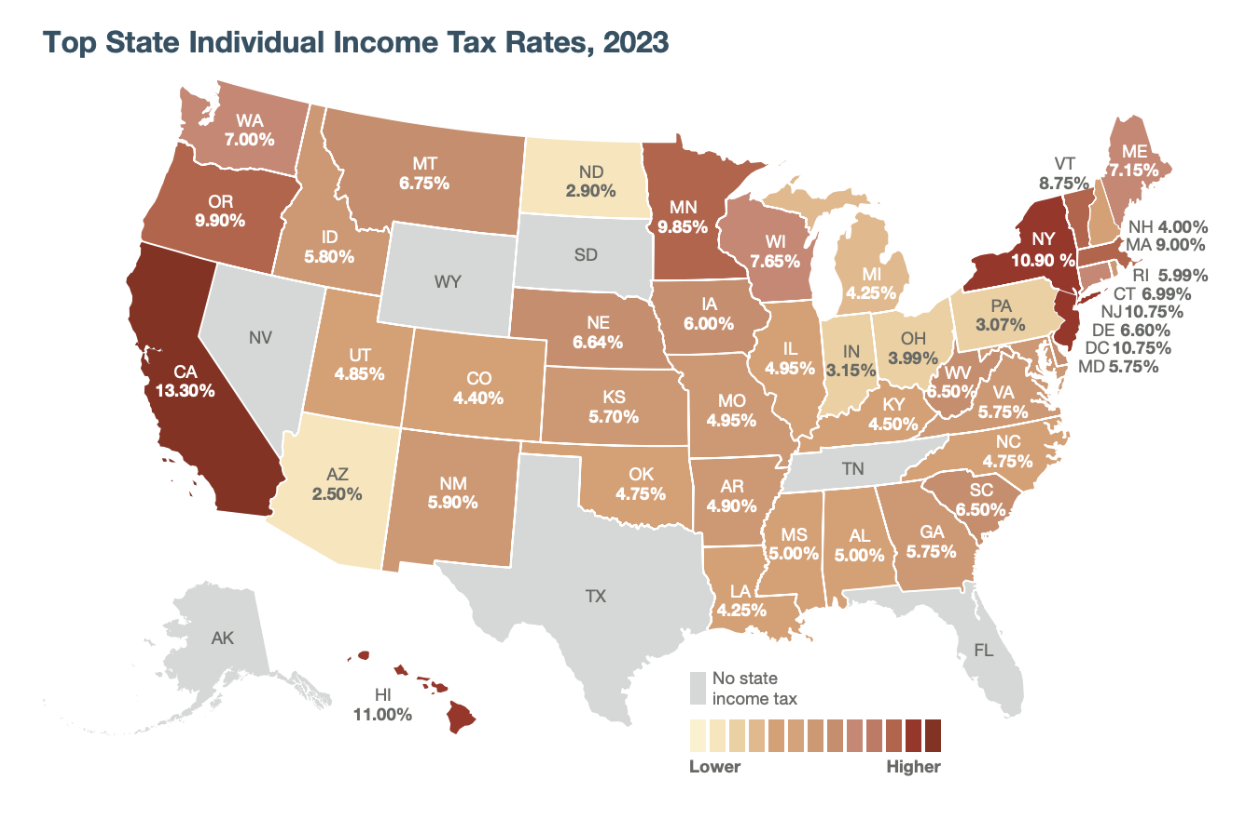

BENEFITS OF STATE TAX-DEFERRAL

Since annuities are both federal and state income tax deferred, a client can combine both income tax rates to determine their overall tax-equivalent yield.

Source: Taxfoundation.org, February 2023. Map shows top marginal rates: the maximum statutory rate in each state. This map does not show effective marginal tax rates, which would include the effects of phase-outs of various tax preferences. Local income taxes are not included.

For instance, if a client is in the 32.0% federal income tax bracket and lives in New York City, the combined income tax rate would be 42.7% (using the New York State income tax rate of 6.85% and the New York City income tax rate of 3.876%).

Combined Federal, State, City Tax Rate

The TEY calculation would be: TEY = Yield / (1 – 42.7%)

Solving for Yield:

Yield = 6.15% / (1 – 0.427)

Yield = 0.0615% / 0.573

Yield = 0.1073 or 10.73%

In this example, your taxable investment would need to yield approximately 10.73% to be equivalent to a 6.15% tax-deferred yield highlighting the additional impact of state tax–advantaged products.

CONCLUSION

When considering a tax-deferred product, such as a MYGA, a client may forget that the yield on this type of product is not directly comparable to the yield on a taxable security. In fact, you can’t really make a direct comparison between an insurance product and an investment in securities — it’s all apples and oranges. But it’s an important part of the conversation to have when discussing the benefits of an overall diversified portfolio — especially when adding a guaranteed product into the lineup for retirement.

Taxable Equivalent Yield is a valuable tool for advisors to help clients assess the impact of taxes on investment returns and tax-deferred alternatives. The higher the tax bracket, the greater the taxable yield needs to be to match the return of a tax-deferred investment or product. It’s essential to consider a client’s tax situation when making decisions to optimize returns and achieve financial goals.

Remember that while TEY provides a helpful comparison, it’s just one factor to consider. Risk, liquidity, and a client’s overall financial strategy should also influence investment and product choices.

Erick

VP of Annuity Sales

Erick Lindewall is an industry veteran with 30 years of experience, including over 20 years as an External Variable Annuity Wholesaler. He as worked with financial advisors in all major distribution channels. Erick has been recognized as a sales and relationship management leader multiple times during his wholesaling career.